Introduction

Student loans are an integral part of higher education financing for many individuals. While they offer an opportunity to pursue academic goals, their long-term impact on personal financial health is significant. Understanding these impacts is essential for making informed decisions about borrowing and repayment strategies.

The Growing Dependence on Student Loans

The cost of higher education has risen dramatically over the past few decades, prompting an increasing reliance on student loans. According to studies, the average cost of tuition and fees has outpaced inflation, making it difficult for families to cover these expenses without external financial assistance. As a result, student loans have become a primary tool for funding college education. However, the convenience of borrowing often masks the challenges of repayment, which can persist for decades after graduation.

Initial Financial Burden

Student loans create an immediate financial burden for borrowers. Upon graduation, individuals are often faced with substantial debt that must be repaid over time. The pressure to start repayment begins shortly after completing education, leaving little time for graduates to establish themselves financially. Monthly payments can consume a significant portion of income, affecting the ability to save, invest, or meet other financial goals.

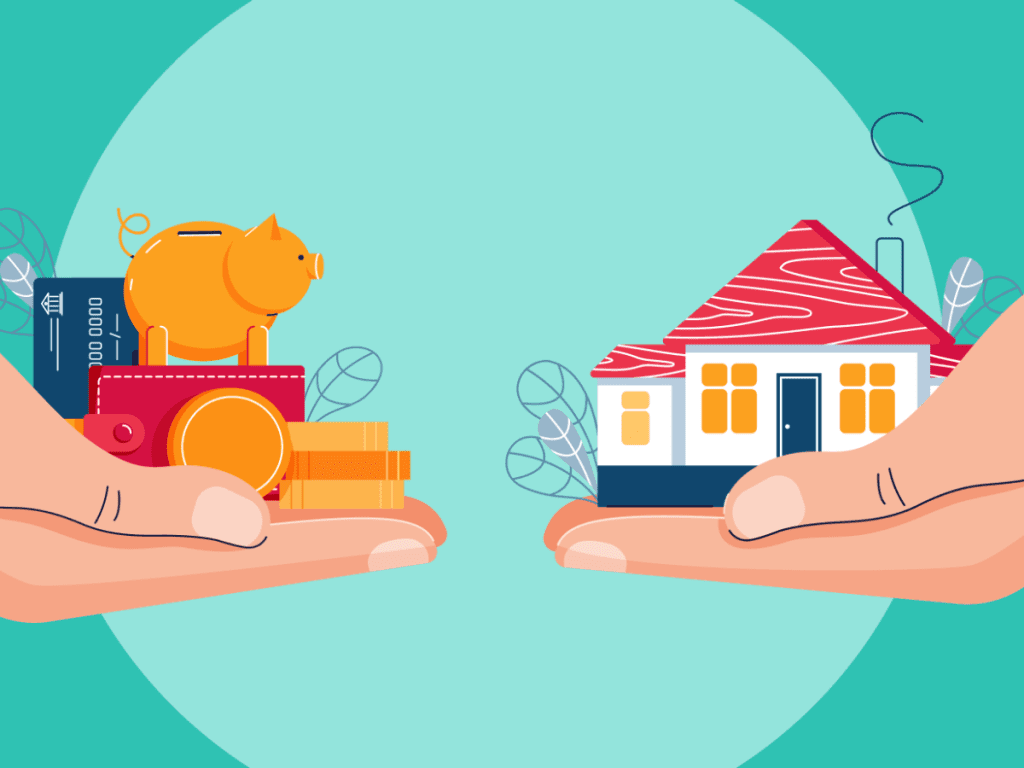

Delayed Financial Milestones

Carrying student loan debt can delay major life milestones, such as purchasing a home, starting a family, or investing in retirement. Many young adults find themselves postponing these decisions due to limited disposable income. For instance, homeownership—a traditional marker of financial stability—often takes a backseat as borrowers prioritize paying off loans. Similarly, retirement savings are frequently neglected, which can have long-term implications on financial security.

Psychological Stress and Well-Being

The stress associated with student loan debt extends beyond finances. Borrowers often experience anxiety and mental health challenges due to the overwhelming responsibility of repayment. The fear of defaulting on loans or falling behind on payments can lead to chronic stress, which negatively affects overall well-being. Research suggests that individuals with high levels of debt are more likely to report symptoms of depression and reduced life satisfaction.

Impact on Career Choices

Student loans influence career decisions, often steering graduates toward higher-paying jobs that may not align with their passions or interests. For many, the need to repay loans outweighs the desire to pursue careers in fields with lower earning potential, such as the arts, non-profit work, or public service. This mismatch can lead to job dissatisfaction and a lack of fulfillment in the long term.

Effects on Credit and Borrowing Capacity

Student loans play a significant role in shaping an individual’s credit profile. Timely repayment positively impacts credit scores, demonstrating financial responsibility to potential lenders. However, missed payments or defaulting on loans can severely damage credit scores, making it challenging to secure other forms of credit, such as mortgages or car loans. Even for borrowers with good repayment habits, high levels of student debt can increase debt-to-income ratios, limiting borrowing capacity for other financial needs.

Economic Ripple Effects

On a broader scale, student loan debt affects the economy. High levels of debt reduce consumer spending power, as borrowers allocate a large portion of their income toward loan repayments. This decreased spending impacts industries that rely on consumer purchases, such as retail and real estate. Additionally, younger generations with significant debt are less likely to invest in businesses or contribute to economic growth, creating a ripple effect on the overall economy.

Loan Forgiveness and Relief Programs

In response to the growing student debt crisis, various loan forgiveness and relief programs have been introduced. These initiatives aim to alleviate the financial burden for specific groups, such as public service employees, teachers, or individuals in low-income brackets. While these programs provide some relief, they are often accompanied by strict eligibility criteria and complex application processes. Understanding the terms and benefits of such programs is crucial for borrowers seeking financial assistance.

Strategies for Managing Student Loan Debt

Effectively managing student loan debt requires a proactive approach. Borrowers should explore repayment options, such as income-driven repayment plans or refinancing, to reduce monthly payments. Budgeting and financial planning are essential for maintaining consistent payments while balancing other financial priorities. Additionally, seeking financial education and professional advice can empower borrowers to make informed decisions and avoid common pitfalls.

The Importance of Financial Literacy

Improving financial literacy is a critical step in addressing the challenges of student loans. Many borrowers enter repayment without a clear understanding of loan terms, interest rates, or repayment options. Educational institutions and policymakers have a responsibility to provide resources that enhance financial knowledge, equipping students with the tools to make informed borrowing decisions. Early education on personal finance can help individuals avoid excessive debt and develop healthy financial habits.

The Role of Policymakers and Institutions

Addressing the impact of student loans requires collaboration between policymakers, educational institutions, and financial organizations. Policymakers should focus on creating affordable education opportunities, reducing reliance on loans. Institutions can contribute by offering transparent cost structures, increasing scholarships, and implementing financial counseling services for students. Financial organizations also play a role by offering fair lending practices and innovative repayment solutions.

Long-Term Implications

The long-term implications of student loan debt extend beyond individual borrowers. As debt levels continue to rise, the broader economic and societal impacts become more pronounced. Reduced consumer spending, delayed wealth accumulation, and limited career mobility collectively influence the financial landscape. Recognizing these implications is essential for developing sustainable solutions that promote financial stability for future generations.

Conclusion

Student loans undoubtedly provide access to education and career opportunities, but they come with significant financial and psychological consequences. Understanding the impact of student loans on personal and economic levels is crucial for borrowers, educators, and policymakers. By adopting proactive strategies, enhancing financial literacy, and fostering systemic change, it is possible to mitigate the challenges associated with student loans and pave the way for a financially secure future.